Columbia Law ReviewTAYLOR SWIFT, TORTURED POETS, AND THE TAX CODE’S FRANKENSTEIN

TAYLOR SWIFT, TORTURED POETS, AND THE TAX CODE’S FRANKENSTEIN

Hilary G. Escajeda*

Taylor Swift’s songs inspire generations of fans to sing and dance about love and to “shake . . . off” heartbreak. Swift’s hard-earned “reputation” for being a savvy music mogul inspires other creative spirits to be “fearless” in their artistic endeavors. But unless these artists are songwriters and musicians, they should keep their “eyes open” when selling their works, as they may see “red” when they discover their tax rates.

The simple fact is that a taxpayer’s financial ability to live out their “wildest dreams” may turn on their chosen artistic medium. Notably, the Internal Revenue Code taxes the sale of poems differently than the sale of songs. As a result, in most cases, poets will be subject to ordinary income tax rates, while songwriters may be eligible for preferential capital gains treatment.

This Piece explores how U.S. tax laws breed “bad blood” between poets and songwriters who sell their creative work products. It then argues that sound public policy requires Congress to take responsibility for the “tax Frankenstein” it has created by articulating consistent policies for taxpayers who sell or dispose of their artistic works.

The full text of this Piece can be found by clicking the PDF link to the left.

* Associate Professor, Mississippi College School of Law. I am grateful for the support of my home institution—the Mississippi College School of Law. This project benefited from workshops both there and at the California State University, Northridge’s Bookstein Institute Tax Development Conference. I dedicate this Piece to my brilliant Swiftie-nieces, Teah and Zinnia. I especially thank Denise Dantzler, Esq., for her thoughtful insights on this project. This Piece flowed from a fusion of ideas inspired by Dr. Catherine Burroughs, whose dramatic readings of Keats, Shelley, and Byron’s poems and thoughtful critique of Mary Shelley’s Frankenstein have resonated with me for many decades.

Introduction

Swift’s love songs often explore the dark side of relationships. For example, in her 2014 song “Wildest Dreams,” Swift sings of a man of bad character:

He’s so tall and handsome as hell

He’s so bad, but he does it so well.

1

Taylor Swift, Wildest Dreams, on 1989 (Big Machine Recs. 2014).

According to the New York Times, the artwork for Swift’s recent album, The Tortured Poets Department, evokes the passion, pain, and fury uncorked by the Romantic poet Lord Byron—the “international heart-throb whose subversive ‘under look’ gave women palpitations” and prompted a jilted lover to burn his picture in a public spectacle.

2

Fiona MacCarthy, Byron: Life and Legend 164 (2002) (internal quotation marks omitted) (quoting Lady Caroline Lamb’s melodramatic diary entry after meeting Lord Byron); Emma Madden, What Tortured Poets Think About Taylor Swift’s Album Title, N.Y. Times (Feb. 6, 2024), https://www.nytimes.com/2024/02/06/style/taylor-swift-tortured-poets-department-album.html (on file with the Columbia Law Review) https://www.nytimes.com/2024/02/06/style/taylor-swift-tortured-poets-department-album.html(describing Swift’s social media announcement posts for the album as “Lord Byron-esque artwork: a gray-scale photo of Swift, spread across a bed in luxurious anguish”). After first meeting Lord Byron (George Gordon), Lady Caroline Lamb’s diary entry described him as “mad—bad—and dangerous to know.” MacCarthy, supra (internal quotation marks omitted). Drawn to his dark flame, Lady Caroline’s short-lived, sizzling romance with Byron ended with her burning “effig[ies]” of his pictures. Id. at 191.

Almost two hundred years later, Swift’s country song lyrics in Picture To Burn elicit similar rage and resentment, but this time against a “redneck heartbreaker” driving a pickup truck.

3

Swift writes:

So go and tell your friends that I’m obsessive and crazy

***

So watch me strike a match

On all my wasted time

As far as I’m concerned, you’re

Just another picture to burn

***

Burn, burn, burn, baby, burn

You’re just another picture to burn

Baby, burn

Taylor Swift, Picture to Burn, on Taylor Swift (Big Machine Recs. 2006); Taylor Swift, Picture to Burn, Musixmatch, https://www.musixmatch.com/lyrics/Taylor-Swift/Picture-to-Burn [https://perma.cc/89A3-5SNP] (last visited Oct. 18, 2024).

Like the eighteenth-century Romantic writers whose poems expressed life’s images as universal truths,

4

Percy Bysshe Shelley, A Defence of Poetry (1821), reprinted in English Romantic Writers 1131, 1134 (David Perkins ed., 2d ed. 1967) [hereinafter Shelley, A Defence of Poetry] (“A poem is the very image of life expressed in its eternal truth.”).

Swift’s twenty-first-century songs shape culture and galvanize the hearts and minds of her devoted and enthusiastic fans—the “Swifties.”

5

Swifties, Wikipedia, https://en.wikipedia.org/wiki/Swifties [https://perma.cc/25WF-MCM2] (last visited Oct. 18, 2024) (describing the “Swifties” as “one of the largest, most devoted, and influential fan bases” who are known for their “cultural impact on the music industry and popular culture”).

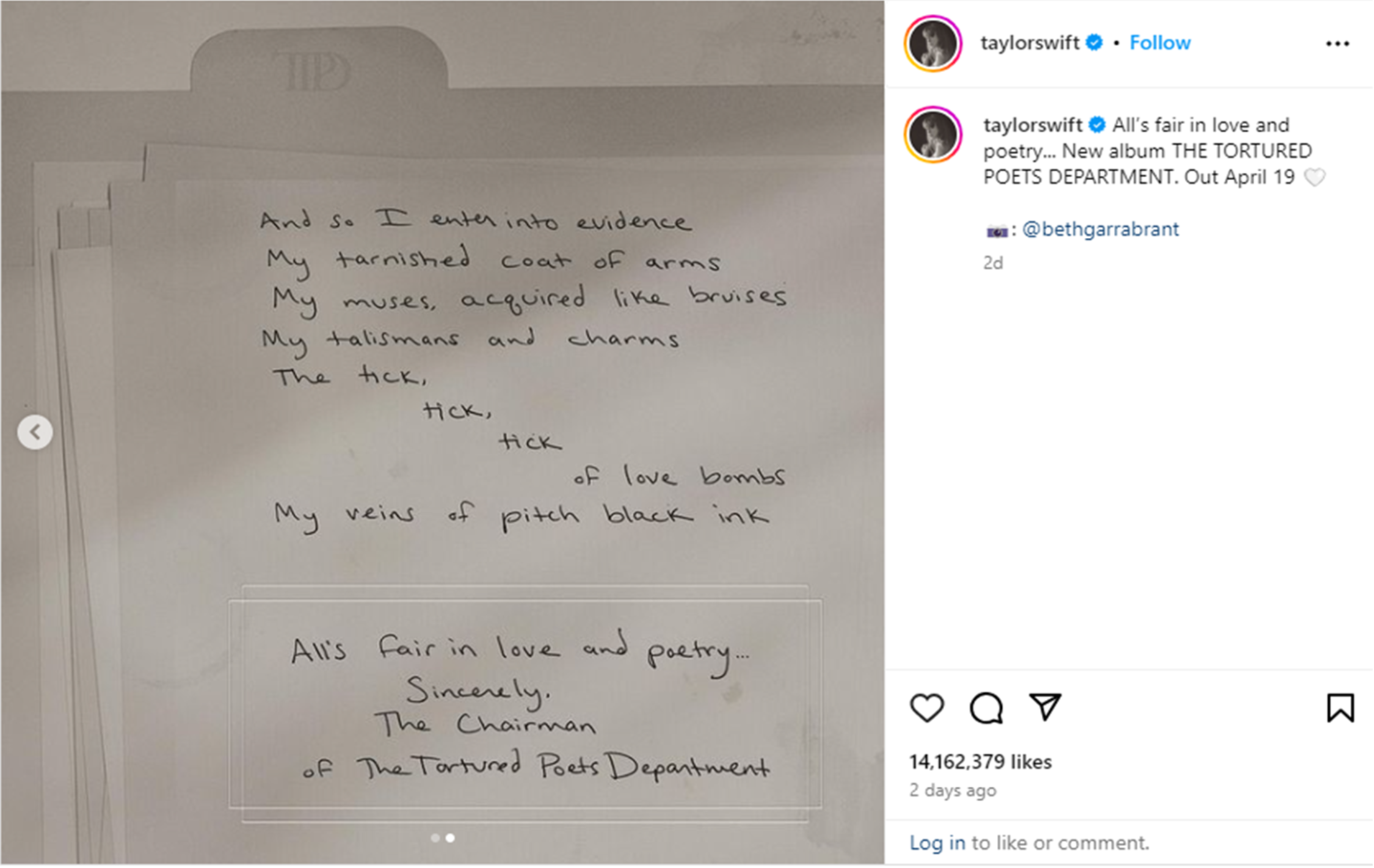

Provoked by Swift’s February 2024 proclamation, “All’s fair in love and poetry,”

6

Taylor Swift (@taylorswift), Instagram (Feb. 4, 2024), https://www.instagram.com/p/C28vsIzO_bL/?hl=en&img_index=2 [https://perma.cc/

6BCM-VGDX] [hereinafter Swift, Instagram].

it has become this author’s nerdy tax mission—as an English-major-turned-tax law professor—to highlight and amplify a curious dysfunction in U.S. tax law that treats the sale of songs more favorably than the sale of poetry. This Piece explores that dichotomy, particularly questioning why the U.S. tax code makes such a distinction between poets and songwriters, who are similarly situated in terms of their creative work.

Part I reveals the artistic nuances that differentiate songs from poetry by delving into the basic contours of literary, musical, and artistic compositions. Understanding these subtle distinctions assists in unraveling the U.S. tax code’s divergent treatment of songs and poetry.

Part II then breaks down the language and history of the Internal Revenue Code (I.R.C.) section 1221, which defines capital assets.

7

Section II.D examines the special tax election for the sale or exchange of self-created musical works in I.R.C. § 1221(b)(3) (2018).

It next questions whether it makes sense to subject poets—artists who sell verses without music—to higher ordinary income tax rates, while songwriters—artists who sell verses with music—may elect to be taxed at lower capital gains rates.

8

Merriam-Webster defines a “verse” as “a composition using rhythm and often rhyme to create a lyrical effect.” Verse, Merriam-Webster, https://www.merriam-webster.com/thesaurus/verse [https://perma.cc/458B-7EPP] (last visited Oct. 18, 2024). Merriam-Webster defines a “poem” as “a composition in verse” or “something suggesting a poem (as in expressiveness, lyricism, or formal grace).” Poem, Merriam-Webster, https://www.merriam-webster.com/dictionary/poem [https://perma.cc/84NE-SQPX] (last visited Oct. 18, 2024). Merriam-Webster defines “lyric” as “a lyric composition, specifically: a lyric poem” or “the words of a song.” Lyric, Merriam-Webster, https://www.merriam-webster.com/dictionary/lyric [https://perma.cc/D7PG-TLA5] (last visited Oct. 18, 2024). Merriam-Webster defines “song” first as “a short musical composition for the human voice often with instrumental accompaniment,” and second as “a composition using rhythm and often rhyme to create a lyrical effect.” Song, Merriam-Webster, https://www.merriam-webster.com/thesaurus/song [https://perma.cc/G89S-2TRS] (last visited Oct. 18, 2024).

Part III briefly considers Mary Shelley’s Frankenstein or, The Modern Prometheus,9

See Mary Wollstonecraft Shelley, Frankenstein or, the Modern Prometheus 52−53 (James Rieger ed., 1982) (1818) [hereinafter Shelley, Frankenstein] (describing Victor Frankenstein’s horror at the physical dissonance of his creation); see also Joyce Carol Oates, Frankenstein’s Fallen Angel, 10 Critical Inquiry 543, 545 (1984) (describing the enduring fame of the Frankenstein legend and emphasizing the ethical implications of creating a “Frankenstein monster” (internal quotation marks omitted)). Joyce Carol Oates explains that, despite “popular misconceptions,” Frankenstein is “not the monster”—Frankenstein is the creator. Id. at 548.

as a means for evaluating the dissonance and dysfunction U.S. tax laws impose on creative works. It contends that the current tax code constitutes a “tax Frankenstein” that treats creative artists inequitably and urges Congress to take responsibility for its mutant creation.

10

See Fiona Sampson, In Search of Mary Shelley: The Girl Who Wrote Frankenstein 4 (2018) (explaining “‘the Frankenstein idea’ . . . that if humans play God with the ‘instruments of life’ they will produce something monstrous”); cf. Shelley, Frankenstein, supra note 9, at 195−98 (opining that humans are always responsible for their engineered creations).

It then asks practical questions for Congress to consider when evaluating fair and consistent policies for artist-taxpayers. This Piece concludes by arguing that Congress must slay its tax monster and treat artistic works equitably.

* * *

So, if “[a]ll’s fair in love and poetry,” then why is all not fair in love and taxes?

11

Swift, Instagram, supra note 6. After Scooter Braun purchased her master recordings, Swift is fully aware of the value of her musical works. See Anne Steele, Taylor Swift’s Early Music Catalog Changes Hands Again, Wall St. J. (Nov. 16, 2020), https://www.wsj.com/articles/taylor-swifts-early-music-catalog-changes-hands-again-11605582712 (on file with the Columbia Law Review) (“Ms. Swift, who has been vocal about her disapproval of the sale of her work to Mr. Braun, said Monday in a statement on Twitter that she had tried to buy her old catalog . . . .”). Swift’s savvy business advisors also most likely recognize that Swift’s artistic medium provides her “poetry” set to music with significant tax advantages under I.R.C. § 1221(a)(3) and (b)(3).

I. ARTISTIC COMPOSITIONS

As discussed below, the taxation of artistic compositions turns on their classification as a literary, musical, or other artistic work.

12

I.R.C. § 1221. Section (a)(3) excludes “literary, musical, or artistic composition[s]” held in certain situations from the term “capital asset.” Id.

Because this Piece focuses on the disparate tax treatment of compositions of poetry, songs, and music, studying each term—like notes on sheet music—aids in critical assessment.

A. Compositions

“Composition” is defined as the “act or process of composing” by merging mental or artistic labor.

13

Merriam-Webster defines “composition” as “the act or process of composing.” Composition, Merriam-Webster, https://www.merriam-webster.com/dictionary/

composition [https://perma.cc/Z3G2-8TA2] (last visited Oct. 21, 2024). “Composing” involves “creat[ing] by mental or artistic labor.” Composing, Merriam-Webster, https://www.merriam-webster.com/dictionary/composing [https://perma.cc/2YMA-PHDU] (last visited Oct. 21, 2024).

Writer and literary scholar Dr. Lavelle Porter explains that the word “composition” describes the intimate relationship between “a work of words or of sounds.”

14

Lavelle Porter, ‘My Music Is Words’: Sun Ra’s Poetry Offers Insight Into the Musician and the Man, Poetry Found. (Feb. 5, 2018), https://www.poetryfoundation.org/articles/145383/my-music-is-words [https://

perma.cc/L59W-GPMY].

Since prehistoric times, humans have combined words and sounds to produce “oral composition[s]” that convey narratives with “set words, word patterns, [and] refrains.”

15

M.H. Abrams & Geoffrey Galt Harpham, A Glossary of Literary Terms 264–65 (11th ed., 2013).

Singers and reciters often performed their oral poetry with a drummer or harpist.

16

Id.

Some early examples of oral poetry compositions include narrative forms, such as epics and ballads, along with lyric (short poem) forms, such as folk songs.

17

Id. at 264. The term “lyric” refers to “any fairly short poem uttered by a single speaker, who expresses a state of mind or a process of perception, thought, and feeling.” Id. at 202. The term has evolved over time. For example, in Greek, a song performed to the accompaniment of a lyre is a “lyric.” Id. at 203. Current usage of term “lyric” sometimes “retains the sense of a poem written to be set to music.” Id.

B. Literary, Musical, and Other Artistic Works

Despite establishing starkly different tax outcomes for literary, musical, and other artistic works, the U.S. tax code lacks definitional guidance.

18

As discussed in Part III, “other artistic works” most likely serves as a catchall provision for works that do not fall neatly within these categories. See infra Part III.

While not definitive, its neighbor, Title 17–Copyrights, offers some insight into the possible meaning of literary and musical works. In particular, § 101 defines “literary works” as “works, other than audiovisual works, expressed in words, numbers, or other verbal or numerical symbols or indicia, regardless of the nature of the material objects, such as books, periodicals, manuscripts, phonorecords, film, tapes, disks, or cards, in which they are embodied.”

19

17 U.S.C. § 101 (2018).

Though “musical works” are not defined in § 101,

20

Congress has explained that this phrase has a “fairly settled meaning[].” See Robert Kastenmeier, Copyright Law Revision, H.R. Rep. No. 94-1476, at 53 (1976).

§ 102 acknowledges a distinction between “literary works” and “musical works, including any accompanying words” when describing works of authorship categories.

21

17 U.S.C. § 102 (emphasis added).

The recognition among artists, scholars, and critics of the integral relationship between words and sounds in artistic compositions further illustrates the overlap between literary and musical works.

22

See supra note 14 and accompanying text.

For example, following the widespread adoption of the printing press,

23

See John Man, The Gutenberg Revolution: The Story of a Genius and an Invention that Changed the World 2 (2002) (“Gutenberg’s invention made the soil from which sprang modern history, science, popular literature, the emergence of the nation-state, so much of everything by which we define modernity.”).

artists often composed their works for print distribution,

24

See Abrams & Harpham, supra note 15, at 271 (“Since the seventeenth century, poetry—like other forms of literature—has been composed primarily for printing.”).

thereby broadcasting their creative voices to readers and performers around the world.

25

See Man, supra note 23, at 291–92 (observing that “Gutenberg’s invention had created the possibility of an intellectual genome, a basis of knowledge which could be passed on from generation to generation, finding expression in individual books”).

Notwithstanding the power of written texts, oral poetry compositions continued to boom and blend with music, as demonstrated by the blues, beat, hip-hop, and rap music genres.

1. Blues and Beats. — Despite the proliferation of printed texts since the seventeenth century,

26

Abrams & Harpham, supra note 15, at 271.

the melding of oral poetry performances continued. For instance, Langston Hughes’s The Weary Blues combined poetry with the blues to forge the “fusion genre known as jazz poetry.”

27

See Rebecca Gross, Jazz Poetry & Langston Hughes, Nat’l Endowment for the Arts (Apr. 11, 2014), https://www.arts.gov/stories/blog/2014/jazz-poetry-langston-hughes [https://perma.cc/G9CE-KQVY] (“Hughes’s love for the music found its way to the page, giving rise to the fusion genre known as jazz poetry.”); see also Langston Hughes, The Weary Blues (1926), Poetry Found., https://www.poetryfoundation.org/poems/47347/the-weary-blues [https://perma.cc/G9CE-KQVY]. Here is an excerpt:

Droning a drowsy syncopated tune,

Rocking back and forth to a mellow croon,

I heard a Negro play.

Down on Lenox Avenue the other night

By the pale dull pallor of an old gas light

He did a lazy sway. . . .

He did a lazy sway. . . .

To the tune o’ those Weary Blues.

With his ebony hands on each ivory key

He made that poor piano moan with melody.

O Blues!

Swaying to and fro on his rickety stool

He played that sad raggy tune like a musical fool.

Sweet Blues!

Coming from a black man’s soul.

O Blues!

Id. According to Gross, “When he wrote about jazz, Hughes often incorporated syncopated rhythms, jive language, or looser phrasing to mimic the improvisatory nature of jazz; in other poems, his verse reads like the lyrics of a blues song. The result was as close as you could get to spelling out jazz.” Gross, supra; see also The Anthology of Rap, at xxxv (Adam Bradley & Andrew DuBois eds., 2010) (presenting Hughes’s argument that the blues was poetry). Allen Dwight Callahan’s powerful recitation of Hughes’s The Weary Blues poem set to music may be found on YouTube. Project Shift, Poetry by Langston Hughes—The Weary Blues, YouTube (Jan. 20, 2007), https://www.youtube.com/watch?v=KyqwvC5s4n8 [https://perma.cc/4ZX9-D96W]; see also Dave Bonta, The Weary Blues by Langston Hughes, Moving Poems: Poetry in Video Form (Feb. 24, 2009), https://www.movingpoems.com/2009/02/the-weary-blues[https://perma.cc/UU2K-GVSS] (last visited Aug. 5, 2024).

On a similar note, the “Beat writers” of the 1950s and early 1960s often performed their literary works in coffee houses to jazz music.

28

Abrams & Harpham, supra note 15, at 28–29.

The mid-1980s and early 1990s ushered in hip-hop’s “golden age,” which “gifted” modern poets and rappers “a rich cultural inheritance.”

29

Adam Bradley, The Artists Dismantling the Barriers Between Rap and Poetry, N.Y. Times: T-Mag. (Mar. 4, 2021), https://www.nytimes.com/2021/03/04/t-magazine/rap-hip-hop-poetry.html (on file with the Columbia Law Review); see also John McWhorter, Opinion, How Hip-Hop Became America’s Poetry, N.Y. Times (Aug. 22, 2023), https://www.nytimes.com/2023/08/22/opinion/hip-hop-anniversary-poetry.html (on file with the Columbia Law Review) (“Rap is verse poetry, in all of its verbal richness and rhythmic variety, a deft stylization of speech into art.”). Professor John McWhorter then explains that “rap” or “rapping” is “a subset of the broader cultural phenomenon of hip-hop, encompassing M.C.ing style, graffiti and dance, as well as the rapping itself.” Id.; see also Abrams & Harpham, supra note 15, at 272 (explaining that since the 1980s, “hip-hop” refers to “a cultural movement among urban African-American youths that originated in New York and was marked by distinctive clothing, graffiti, break dancing, and music, especially rap”).

2. Hip-Hop and Rap. — Scholars now consider hip-hop and rap as lyric performance poetry, “primarily experienced as music.”

30

See The Anthology of Rap, supra note 27, at xxxv; see also Abrams & Harpham, supra note 15, at 272.

Professors Amber West and Adam Bradley describe rap as a hybrid art form that combines poetry and music

31

See Cynthia Lee, Rap Lyrics as Literature, UCLA Mag. (Feb. 15, 2022), https://newsroom.ucla.edu/magazine/lectures-lyrics-hip-hop-rap-poetry [https://

perma.cc/G6KW-7G4P] (describing West’s and Bradley’s scholarly work on the poetry and rhythms of rap and hip-hop). West explains how rappers’ works employ the traditional poetry techniques of metaphor, imagery, simile, rhyme, rhythm, and careful attention to language. See id.

by employing poetry’s “[e]conomy of language” along with repetitive words and sound.

32

Bradley,supra note 29.

Atlanta-based rapper Latto declared that “[r]ap is definitely poetry . . . . We just do it on top of a beat.”

33

Id (internal quotation marks omitted) (quoting Latto). Bradley explains that “a line of demarcation persists between rap and poetry, born of outmoded assumptions about both forms: that poetry only exists on the page and rap only lives in the music, that poetry is refined and rap is raw, that poetry is art and rap is entertainment.” Id. His article also describes how artists incorporate hip-hop samples into their verses—an action that can transform these poets’ and rappers’ art into a “political act.” See id.

For artists like Khadijah Queen “and other Black poets, hip-hop is not only beats and rhymes” but also the creation of a “space” for artists to speak and be themselves without censorship or shame.

34

Id (internal quotation marks omitted) (quoting Queen).

Interestingly, much like medieval balladeers, modern rap artists often perform their lyrics live before writing them down for public consumption and wide distribution.

35

See The Anthology of Rap, supra note 27, at xlvi.

For more than three decades, scholars and critics have heralded Lauryn Hill for the “sharpness and innovation of her rhymes.”

36

Id. at xli, 410 (describing Hill as a beloved and enigmatic hip-hop artist who is “one of the most musical of rappers”). For further insight into Hill’s musical legacy, see Hannah Giorgis, The Complicated Female Genius of Lauryn Hill, The Atlantic (Aug. 27, 2018), https://www.theatlantic.com/entertainment/archive/2018/08/the-complicated-female-genius-of-lauryn-hill/568612 [https://perma.cc/D9PU-AK6L] (describing Hill as an “unlikely heroine” with “stellar lyricism” that has “granted her access to a title most often assigned to men: genius”).

The first four lines of Hill’s “Lost Ones” (1998) underscore her poetic and musical genius:

It’s funny how money changes situations

Miscommunication lead to complication

My emancipation don’t fit your equation

I was on the humble, you on every station

37

The Anthology of Rap, supra note 27, at 412.

Here, in Hill’s lyrics, one reads and hears layers of melody, alliteration, and rhyme “both at the end and within the line.”

38

Id. at 410.

A little over two decades later, another female artist, Rapsody, has taken over the spotlight. Rapsody’s lyrics “have earned [her] the reputation among [both] peers [] and . . . poets [] as one of the most innovative lyricists in the game.”

39

Bradley, supra note 29. Rapsody has compared rap to math because it challenges her to connect metaphors from the beginning, through the middle, and to the end of the piece. Id.

Since the 2019 release of Rapsody’s critically acclaimed album Eve, “hip-hop purists” have “debat[ed] her potentially rivaling Kendrick Lamar for the lyrical throne.”

40

Gary Gerard Hamilton, Rapsody’s Brave New Album, ‘Please Don’t Cry,’ Displays Strength Through Vulnerability, The AP (May 24, 2024), https://apnews.com/article/rapsody-please-dont-cry-f2dec85e48067040ef75a56210302f0a (on file with the Columbia Law Review).

Incidentally, Kendrick Lamar earned both critical acclaim and the 2018 Pulitzer Prize in Music for his rap album, DAMN.—once again blurring the boundary between poetry and music.

41

See Lee, supra note 31.

3. Poetry and Sound. — Long before rap artists commanded center stage, artists recognized the inseparable connection between poetry, sound, song, and music.

42

For example, Percy Bysshe Shelley wrote, “A poet is a nightingale, who sits in darkness and sings to cheer its own solitude with sweet sounds; his auditors are as men entranced by the melody of an unseen musician, who feel that they are moved and softened, yet know not whence or why.” Shelley, A Defence of Poetry, supra note 4, at 1135.

For instance, John Keats’s nineteenth-century poem Hyperion43

John Keats, Hyperion, Poetry Found., https://www.poetryfoundation.org/

poems/44473/hyperion [https://perma.cc/S29Y-D8YD] (last visited Oct. 24, 2024). Excerpt from Book I:

Deep in the shady sadness of a vale

Far sunken from the healthy breath of morn,

Far from the fiery noon, and eve’s one star,

Sat gray-hair’d Saturn, quiet as a stone,

Still as the silence round about his lair;

Forest on forest hung about his head

Like cloud on cloud.

Id.

masterfully marries music and melody to depict a “dethroned Satan in his melancholy solitude.”

44

2 The Keats Circle: Letters and Papers 1816–1878, at 277–78 (Hyder Edward Rollins ed., 1948). Rollins further observed how Keats was “a master of melody” by managing open and closed vowel sounds like “notes of music to prevent monotony.” Id.

Also amplifying the cohesiveness of poetry, sound, song, and music, Sun Ra—poet, “jazz innovator,” and “cosmic bandleader”—wrote, “My music is words and my words are music.”

45

Porter, supra note 14 (quoting Sun-Ra, My Music is Words, 1 Cricket: Black Music in Evolution, no. 1, 1968, at 27, 30).

Similarly, Sun Ra’s 1966 poem, The Neglected Plane of Wisdom, states that “music is a universal language” and asserts that “Freedom of Speech is Freedom of Music.”

46

Id. Here is an excerpt from Sun Ra’s poem, The Neglected Plane of Wisdom:

Music is a plane of wisdom, because music is a universal

language, it is a

language of honor, it is a noble precept, a gift of

Airy

Kingdom, music is air, a universal existence . . .

common to all the

living.

Music is existence, the key to the universal language.

Because it is the universal language.

Freedom of Speech is Freedom of Music.

Id.

Literary critics, likewise, recognize the essential connection between words and sound. In his book, The Fourth Dimension of a Poem: And Other Essays, Professor M.H. Abrams stresses that “poets, whether deliberately or unconsciously, exploit the physical aspect of language” and that this happens through “the act of . . . utterance” by the human voice.

47

M.H. Abrams, The Fourth Dimension of a Poem: And Other Essays 2 (2012). Abrams explains that the first dimension is visual, the second includes the sounds when the words are imagined or read aloud, the third represents the meaning of such words when read or heard, and the fourth dimension “is the activity of enunciating the great variety of speech-sounds that constitute the words of a poem.” Id.

He explains:

It is easy to overlook the fact that a poem, like all art forms, has a physical medium, a material body, which conveys its nonmaterial meanings. That medium is not a written or printed text. The physical medium is the act of utterance by the human voice, as it produces the speech-sounds that convey a poem. We produce those sounds by varying the pressure on the lungs, vibrating or stilling the vocal cords, changing the shape of the throat and mouth, and making wonderfully precise movements of the tongue and lips.

48

Id.

Professor Abrams further emphasizes that the fourth dimension—vocal expression—is vital to the moods and meanings poems convey.

49

See id. at 2–3 (“[T]he oral actions that body forth the words of a poem, even when they remain below the level of awareness, may serve, in intricate and diverse ways, to interact with, confirm, and enhance the meanings and feelings that the words convey.”).

Bob Dylan’s 2016 Nobel Prize in Literature resolved the debate about whether song lyrics are literature; Dylan’s creation of “new poetic expressions within the great American song tradition” motivated the Nobel Committee to award Dylan the prize.

50

See Bob Dylan–Facts, The Nobel Prize, https://www.nobelprize.org/prizes/literature/2016/dylan/facts [https://perma.cc/

V3N5-W2EQ] (last visited Oct. 20, 2024). The Nobel Prize website describes how Dylan’s songs united the “tradition of American folk music” with “the poets of modernism and the beatnik movement.” Id. In addition, “Dylan’s lyrics incorporated social struggles and political protest” into “refined rhymes” and “surreal imagery.” Id.

In summary, artists, scholars, and critics alike recognize the overlap between literary and musical works. But, as explained in Part II, the tax code does not.

II. TAX TREATMENT OF ARTISTIC COMPOSITIONS

A. Income Types: Ordinary and Capital

The sale or disposition of assets may result in the seller’s recognition of taxable gains or losses.

51

I.R.C. § 1001 (2018).

Asset type determines the applicability of higher ordinary income or lower capital gains taxes.

52

I.R.C. § 64. Section 64 defines ordinary income as “any gain from the sale or exchange of property which is neither a capital asset nor property described in section 1231(b).” Id. Section 1231(b) applies to “property held by the taxpayer primarily for sale to customers in the ordinary course of his trade or business.” I.R.C. § 1231(b)(1)(B). For an excellent article discussing these issues, see generally Xuan-Thao Nguyen & Jeffrey A. Maine, Taxing Creativity, 89 Tenn. L. Rev. 523 (2022) (describing the historical treatment of created works as ordinary assets).

The I.R.C. taxes gains from ordinary assets at rates between ten and thirty-seven percent and gains from capital assets at rates between zero and twenty-eight percent.

53

I.R.C. § 1. It is worth noting that these artists may be subject to self-employment taxes. For instance, section 1401 imposes up to a 15.3% tax on self-employment income for that taxable year. I.R.C. § 1401. In section 1402(a)(3)(A), however, the I.R.C. excludes any gains or losses that are “considered as gain or loss from the sale or exchange of a capital asset.” I.R.C. § 1402(a)(3)(A).

Because taxpayers typically want to minimize their tax liabilities, they often seek opportunities to convert ordinary assets into capital assets.

54

See Nguyen & Maine, supra note 52, at 542. Preferential capital gains tax rates reduce taxpayers’ income tax liabilities and are considered “tax expenditures.” See Joint Comm. on Tax’n, JCX-23-20, Estimates of Federal Tax Expenditures for Fiscal Years 2020–2024, at 2 (2020).

I.R.C. § 1221(a) defines capital assets and eight types of property that are not capital assets (i.e., ordinary assets).

55

See I.R.C. § 1221(a). I.R.C. § 1221(a) states that “the term ‘capital asset’ means property held by the taxpayer (whether or not connected with [their] trade or business).” Id. The § 1221(a) exceptions include: (1) inventory; (2) depreciable property; (3) self-created work products such as patents, inventions, models or designs, secret processes or formulas, copyrights, artistic compositions (including literary and musical), letters and memoranda, or other property; (4) accounts or notes receivable; (5) U.S. government publications; (6) commodities derivative financial instruments; (7) hedging transactions; and (8) supplies. Id.

For artist-taxpayers whose “personal efforts” create outputs they eventually sell, the classification of their work products as either capital or ordinary assets dictates their tax rates.

56

Id. § 1221(a)(3).

This interplay between I.R.C. § 1221(a)(3) and 1221(b)(3) sets the range and tone for this Piece’s analysis of the tax disparities among self-created artistic works.

B. General Rules for the Sale or Exchange of Artistic Works

As briefly noted above, the I.R.C. defines capital assets in the negative; that is, it enumerates what is not a capital asset.

57

See Steven T. Black, Capital Gains Jabberwocky: Capital Gains, Intangible Property, and Tax, 41 Hofstra L. Rev. 359, 393 (2012) (observing that the capital asset “definition was written in the negative”); Rodney P. Mock & Jeffrey Tolin, I Should Have Been a Rockstar: Deconstructing Section 1221(a)(3), 65 Tax Law. 47, 51 (2011) (describing items of income excluded from capital gains treatment under § 1221); Nguyen & Maine, supra note 52, at 543 (observing that the definition of a capital asset is a “mess” and is defined in “negative terms”).

Specifically, I.R.C. § 1221(a) states that a capital asset does not include:

(3) a patent, invention, model or design (whether or not patented), a secret formula or process, a copyright, a literary, musical, or artistic composition, a letter or memorandum, or similar property, held by–

(A) a taxpayer whose personal efforts created such property.

58

I.R.C. § 1221(a) (emphasis added).

An analysis of this statutory language reveals that I.R.C. § 1221(a)(3) defines capital assets as not including several types of taxpayer-created property.

59

See id.

This negative definition of capital assets means that literary, musical, or artistic compositions constitute ordinary assets.

60

See Black, supra note 57, at 378 (analyzing the tax consequences of the hypothetical sale of a copyrighted novel and concluding that the author is subject to ordinary income tax rates).

Further, as discussed below, I.R.C. § 1221(a)(3) also includes the language “or similar property” as a catchall ordinary asset category, which appears to apply when taxpayers sell their name, image, and likeness (NIL) rights.

61

I.R.C. § 1221(a)(3); Treas. Reg. § 1.1221-1(c)(1) (as amended in 1975) (stating that any property eligible for copyright protection is ineligible for capital gains treatment).

It is worth noting that neither I.R.C. § 1221(a)(3)(A) nor 1221(b)(3) define “self-created musical works.”

62

I.R.C. § 1221(a)(3)(A) (excluding “a taxpayer whose personal efforts created such property”); id. § 1221(b)(3) (providing no definition of the term); see also Michael R. Morris, Songwriters Continue to Score Tax Breaks, Daily J. (June 21, 2023), https://www.dailyjournal.com/articles/373486-songwriters-continue-to-score-tax-breaks [https://perma.cc/FEZ6-KMSG] (noting the lack of definition and identifying some challenges in determining what constitutes self-created musical compositions and works).

Treasury Regulation § 1.1221-1 offers some guidance by explaining that the language “whose personal efforts created such property” requires an analysis of the taxpayer’s contribution to property creation.

63

See Treas. Reg. § 1.1221-1(c)(3).

Such fact-based analyses examine whether (1) the taxpayer affirmatively created or produced the work

64

See id. (stating that works that the taxpayer created satisfy the “personal efforts” requirement, while “merely [exercising] administrative control of writers, actors, artists, or personnel [without] substantially engag[ing] in the direction and guidance of such persons” does not meet the requirement).

or (2) the taxpayer merely exercised administrative control and did not substantially direct or guide the work and actions of others.

65

See id. The regulation then uses a business executive “who merely has administrative control” over creative personnel as an example of when a taxpayer would not create property by their personal efforts. See id.

C. Name, Image, and Likeness Rights

KISS’s spring 2024 sale of its music catalog—plus its distinct NIL rights to its characters and makeup—to Pophouse illustrates the complexity of disentangling the various elements of artistic compositions and their associated taxation.

66

See Daniel Kreps, Kiss Sell Music Catalog, Publishing, and Imagery to Company Behind ABBA Voyage, Rolling Stone (Apr. 4, 2024), https://www.rollingstone.com/music/music-news/kiss-sell-music-catalog-publishing-imagery-deal-pophouse-1234998911[https://perma.cc/93F5-EKBT].

Because tax- and business-savvy musicians would prefer to have the sale of their NIL rights taxed at lower capital gains rates, they may seek to characterize such assets as capital rather than ordinary.

67

See Nguyen & Maine, supra note 52, at 542 (observing that “[m]ost creators would prefer that income generated from their creative works be treated as so called ‘capital gains’”).

I.R.C. § 1221(a)(3), however, appears to preclude such favorable tax treatment of NIL rights under both the “artistic composition” and “or similar property” language.

68

See I.R.C. § 1221(a)(3) (2018); see also Treas. Reg. § 1.1221-1(c)(1) (explaining that “similar property” includes “property eligible for copyright protection”).

Specifically, Gene Simmons’s and Paul Stanley’s characters, “God of Thunder” and “Star Child,” along with their signature face painting and costumes, could be reasonably classified as “artistic composition[s].”

69

See Treas. Reg. § 1.1221-1(c)(1).

Further, the sale of these NIL rights appears to qualify under I.R.C. § 1221(a)(3)’s catchall category of “or similar property.” Under either classification, Simmons and Stanley’s sale of their NIL rights constitutes gross income from the sale of ordinary assets under I.R.C. § 61.

70

See I.R.C. § 61(a) (defining gross income as “all income from whatever source derived”); W. Brian Dowis, R. Lainie Wilson Harris & Gloria Stuart, The Tax Impact and Planning Opportunities of the NIL Rules on Student- Athletes, 138 J. Tax’n 29, 30 (2023) (stating that NIL compensation is covered by the I.R.C. § 61 “whatever source derived” definition). Future litigation of the taxation of NIL rights may involve analyzing the possible categorization of such payments under I.R.C. § 61(a)(6). Under either analysis, the sale or disposition of NIL rights would be gross income under § 61. For an analysis of a deceased artist’s image and likeness rights, see Estate of Jackson v. Comm’r, 121 T.C.M. (CCH) 1320, at *34 (T.C. 2021) (finding that Michael Jackson’s image and likeness were intangible rights transferred after death and, therefore, must be included in his gross estate).

In a nutshell, when artist-taxpayers sell their self-created works, they are generally subject to ordinary income tax rates instead of preferential capital gain tax treatment.

71

See I.R.C. § 1.

For example, painters, sculptors, authors, poets, and other performance artists will recognize gross income for any compensation for services, fees, and royalties received, as well as any gains derived from their business or dealings in property.

72

See I.R.C. § 61(a)(1)–(3), (6).

As a general rule, I.R.C. § 1221(a) ensures that creative artists will be taxed at ordinary income rates—consistent with workers who provide labor and services to their employers and receive wages in return.

73

See Nguyen & Maine, supra note 52, at 546 (“[U]nder fairness principles, both creators and laborers should be taxed the same.”); see also Allen Bargfrede, Music Law in the Digital Age: Copyright Essentials for Today’s Music Business 25–26 (2d ed. 2017) (defining the term “work for hire” as an employer engaging (commissioning) a creator to produce a product, with the employer owning the copyright from inception).

D. Special Election for the Sale or Exchange of Self-Created Musical Works

Between 2001 and 2005, Bart Herbison, executive director of the Nashville Songwriters Association International, orchestrated nearly four hundred visits by songwriters to serenade “every member of the tax-writing committees in the House and Senate” while strumming their guitars.

74

Brody Mullins, Music to Songwriters’ Ears: Lower Taxes, Wall St. J. (Nov. 29, 2005), https://www.wsj.com/articles/SB113322576138408618 (on file with the Columbia Law Review) (describing how Bob Regan, “volunteer president of the songwriters association,” would bring together lawmakers with songwriters who had a “story to tell” (internal quotation marks omitted) (quoting Bob Regan)); see also 1 Alexis de Tocqueville, Democracy in America 411–12 (Henry Reeve trans., Arlington House 1966) (1835) (stating that the United States has “a conciliatory government under which resolutions are allowed time to ripen; and in which they are deliberately discussed, and executed with mature judgment”).

After several years of “delicate”

75

Taylor Swift, Delicate, on Reputation (Big Machine Recs. 2017).

and strategic Capitol Hill lobbying efforts, Representatives Marsha Blackburn of Tennessee and Lloyd Doggett of Texas formed the Songwriters Caucus, which proved instrumental in the 2006 passage of the Songwriters Capital Gains Tax Equity Act.

76

See Mullins, supra note 74 (noting how the Songwriters’ Caucus in the House and Senate framed songwriter sales as tax and business issues); see also David Bernstein, Songwriters Say Piracy Eats Into Their Pay, N.Y. Times (Jan. 5, 2004), https://www.nytimes.com/2004/01/05/business/media-songwriters-say-piracy-eats-into-their-pay.html (on file with the Columbia Law Review) (describing the Nashville Songwriters Association’s lobbying efforts concerning piracy and other industry concerns); Songwriters Capital Gains Repealed in Tax Bill, Then Reinstated, Nashville Songwriters Ass’n Int’l (Nov. 7, 2017), https://www.nashvillesongwriters.com/songwriters-capital-gains-repealed-tax-bill-then-reinstated [https://perma.cc/VLU3-C6NW] (discussing how the Songwriters Capital Gains Tax Equity Act was repealed in 2017 and then reinstated four days later). In June 2023, Representatives Ted Lieu (D-CA) and Ben Cline (R-VA) relaunched the Songwriters Caucus to focus on policies that protect artist works and support the industry. Ashley King, Bipartisan Congressional Songwriters Caucus Relaunched, Digit. Music News (June 25, 2023), https://www.digitalmusicnews.com/2023/06/25/bipartisan-congressional-songwriters-caucus-relaunched/ [https://perma.cc/69W4-G9YR].

The resulting I.R.C. § 1221(b) special tax rules provide:

(3) Sale or exchange of self-created musical works.—At the election of the taxpayer, paragraphs (1) and (3) of subsection (a) shall not apply to musical compositions or copyrights in musical works sold or exchanged by a taxpayer described in subsection (a)(3).

77

I.R.C. § 1221(b)(3); see also Treas. Reg. § 1.1221-3 (2025) (discussing when and how a taxpayer can elect to revoke capital treatment of the sale or exchange of a musical work). The Copyright Act of 1976 provides a copyright owner with six exclusive rights: reproduction, preparation of “derivative works,” distribution, public performance, public display, and public performance of a sound recording in nonexempt digital formats. 17 U.S.C. § 106 (2018); see also Bargfrede, supra note 73, at 18 (discussing the copyright owner’s exclusive rights of reproduction and preparation of derivative works).

Succinctly put, this tax provision grants a particular group of taxpayers (songwriters and musicians) a special election to receive preferential capital gains tax rates on the sale of their musical compositions or copyrights.

78

I.R.C. § 1221(b)(3); Treas. Reg. § 1.1221-3. See generally Joint Comm. on Tax’n, JCX-23-20, Estimates of Federal Tax Expenditures for Fiscal Years 2020–2024, at 2 (Nov. 5, 2020) (defining tax expenditures as including preferential tax rates and special tax provisions for “particular taxpayers”).

E. “Mo Money, Mo Problems”

79

The Notorious B.I.G, Mo Money Mo Problems, on Life After Death (Bad Boy Recs. 1997).

Before the December 2006 passage of the Songwriters Capital Gains Tax Equity Act, songwriters and musicians who sold a royalty stream on a song catalog would be subject to ordinary income tax rates, which at that time exceeded forty percent.

80

I.R.C. § 61(a)(6) (defining royalties as gross income); I.R.C. § 1221(b)(3) (setting out the special rules for the “[s]ale or exchange of self-created musical works”).

Now, after the passage of the I.R.C. § 1221(b)(3) special election, songwriters are eligible for capital gains treatment upon the sale of their song catalogs.

81

A catalog contains an artist’s legal rights and economic revenues in their self-created compositions. Scott Pascucci of Concord explains catalog revenue sources such as those from domestic or international streaming or terrestrial radio. See Drop the Mic: The Business of Music, Milken Inst.,at 29:28–30:01 (May 4, 2022), https://milkeninstitute.org/video/music-business-mic-drop [https://perma.cc/6UJM-2GAP] (stating that the source of revenue streams is a relevant factor in deciding whether to invest in a musician’s catalog). Musician-songwriter taxpayers seeking to sell their works assemble a collection of their compositions and copyrights into a catalog. See Master Music Catalog, Henry Kapono Found., https://www.henrykaponofoundation.org/resources/master-music-catalog [https://perma.cc/N2ZV-CNWB] (last visited Oct. 20, 2024) (explaining that a music catalog “is a comprehensive list of musical compositions and songs that are created and registered under the name of an individual or entity”). The “rights owner” then receives the royalty income from music consumption or use. Id.; see also Mullins, supra note 74 (observing that the capital gains rate applies only to the “sales of ‘song catalogs’—collections of a writer’s work—and not to ordinary royalty income from individual songs”). Following catalog sale, the artists relinquish their copyrights and royalty income in their songs or recordings to the buyer, who then controls the rights to use and reproduce the catalog. Ben Sisario, A $550 Million Springsteen Deal? It’s Glory Days for Catalog Sales., N.Y. Times (Dec. 20, 2021), https://www.nytimes.com/2021/12/20/arts/music/bruce-springsteen-catalog.html (on file with the Columbia Law Review); Kathryn Underwood, How Much Is a Music Catalog Worth? Depends on the Artist, Mkt. Realist (Jan. 26, 2023), https://marketrealist.com/media-and-entertainment/how-much-are-music-catalogs-worth/ [https://perma.cc/6W5A-9DAP].

So, by cataloging and selling their songs, songwriters and musicians can elect to pay a one-time capital gains tax at the maximum rate of twenty percent.

82

See I.R.C. § 1221(b)(3).

In recent years, Bruce Springsteen, Bob Dylan, KISS, Paul Simon, Neil Young, Stevie Nicks, and Cyndi Lauper sold their music catalogs and likely secured advantageous tax treatment under I.R.C. § 1221(b)(3).

83

Beau Stapleton & Burak Ahmed, Capital Gains Election Will Keep Driving Music Catalog Sales, Bloomberg Tax (Jan. 3, 2023), https://news.bloombergtax.com/tax-insights-and-commentary/capital-gains-election-will-keep-driving-music-catalog-sales (on file with the Columbia Law Review) (observing that artists can enjoy “multiples of more than 20 times annual net royalty income” by cataloging and selling their self-made musical works); see also Shirley Halperin, The Ins and Outs of Music Catalog Sales, Explained by the Experts, Variety (June 15, 2022), https://variety.com/2022/music/podcasts/music-catalog-sales-explained-strictly-business-podcast-1235292005/[https://perma.cc/W42Y-GPDZ] (exploring the forces driving catalog sales).

Table 1. Catalog Sales (Estimated)

84

Catalog estimates are derived from multiple sources. See Andy Greene, Neil Young Sells Catalog Rights to Merck Mercuriadis’ Hipgnosis, Rolling Stone (Jan. 6, 2021), https://www.rollingstone.com/pro/news/neil-young-music-catalog-hipgnosis-investment-1110037 [https://perma.cc/U6LN-TPBX]; Hits for Sale: Notable Artists Who Have Had Their Music Catalogs Sell for Big Money, The AP (Apr. 4, 2024), https://apnews.com/article/music-catalog-sales-pop-rock-kiss-springsteen-57df80487ecd6cc6b2229560cd6c2469 (on file with the Columbia Law Review) (describing the Dylan, KISS, Nicks, and Springsteen catalog sales); Robert Levine, Fans Just Want to Have Fun: Cyndi Lauper Sells Majority Share of Rights to Pophouse, Billboard (Feb. 29, 2024), https://www.billboard.com/business/business-news/cyndi-lauper-catalog-sale-pophouse-publishing-song-royalties-1235618559/ (on file with the Columbia Law Review) (noting that the purchaser, Pophouse, did not disclose whether the sale included Lauper’s “name, image and likeness rights”); Simon Read, Neil Young Sells Song Rights in ‘$150m’ Deal, BBC (Jan. 6, 2021), https://www.bbc.com/news/business-55557633 [https://perma.cc/KR2D-JUGB]; Ariel Shapiro, Inside Paul Simon’s Catalog Sale: At $250 Million, It’s One of Music’s Biggest, Forbes (Apr. 30, 2021), https://www.forbes.com/sites/arielshapiro/2021/04/30/inside-paul-simons-catalog-sale-at-250-million-its-one-of-musics-biggest-bob-dylan/ [https://perma.cc/3VY8-D9RV].

Artist

Sale Amount

Bruce Springsteen

$550,000,000

Bob Dylan

$300,000,000–500,000,000

KISS*

$300,000,000

Paul Simon

$250,000,000

Neil Young

$150,000,000

Stevie Nicks

$100,000,000

Cyndi Lauper

Not disclosed

Taken altogether, U.S. law taxes the sale of poems set to music more favorably (capital gains) than poems without music (ordinary income). By enacting the I.R.C. § 1221(b)(3) election, Congress has bestowed a select group of taxpayers—musicians and songwriters—with special tax benefits. I.R.C. § 1221(b)(3) thus evidences an unprincipled approach to tax policy.

III. “Tax Frankenstein”

Mary Wollstonecraft Shelley’s novel Frankenstein or, Modern Prometheus offers a cogent frame of reference for critiquing modern tax policy. In her 1818 text, Shelley argues that humans are responsible for their engineered creations and any resulting harm and destruction.

85

See Shelley, Frankenstein, supra note 9, at 47–54, 194−98 (illustrating Frankenstein facing the consequences of creating his monster).

The U.S. Congress likewise reains responsible for the tax policy mutant it cobbled together for the taxation of artistic works. This Part explores how this “tax Frankenstein” treats certain artist-taxpayers unfairly.

86

Phyllis C. Taite, Saving the Farm or Giving Away the Farm: A Critical Analysis of the Capital Gains Tax Preferences, 53 San Diego L. Rev. 1017, 1037–38 (2016) (“The primary purpose of taxation is to raise revenue; yet, tax preferences reduce revenue. For that reason, policymakers should base any justification for maintaining a tax preference on the benefit to the majority, not a select few.” (footnote omitted)).

It then argues that the I.R.C.’s statutory dissonance can be turned into consonance with principled and coherent adjustments to the Code.

A. Love Stories and Taxes

Human experience roots and sustains music and literature. For instance, Swift’s dulcet tune, Love Story, describes a modern Romeo and Juliet whose “love is difficult but . . . real.”

87

Taylor Swift, Love Story, on Fearless (Big Machine Recs. 2008).

The star-crossed lovers ultimately find love in the song’s crescendo when Romeo proposes marriage with a ring in hand.

88

Id.

As a counterpoint of love never found, Frankenstein describes a concocted creature’s craving for the “love and fellowship” of humans.

89

Shelley, Frankenstein, supra note 9, at 219 (“I, the miserable and the abandoned, am an abortion, to be spurned at, and kicked, and trampled on. Even now my blood boils at the recollection of this injustice.” (internal quotation marks omitted)).

The monster’s feelings of abandonment, rejection, and loneliness ultimately transform him into “a depraved wretch” who enjoys “carnage and misery.”

90

Id. at 72.

While both stories explore love and heartbreak, the discordant tax treatment of these self-created artistic works sounds flat, makes no sense, and unleashes bad “karma.”

91

Taylor Swift, Karma, on Midnights (Republic Recs. 2022).

If the Songwriters Caucus acted in good faith to help its constituents, why does the I.R.C. provide preferential tax treatment only to songwriters and musicians? What separates poets and songwriters?

B. The Poet/Songwriter Distinction

The following example highlights the complexity of the tax code’s treatment of poems, songs, and music. When “art music” composer and Professor Laura Schwendinger employs “tone painting” to convey images and ideas in Sylvia Plath’s poem, Lady Lazarus, through sound,

92

Laura Schwendinger, A Sort of Music, Poetry Mag. (Nov. 20, 2007), https://www.poetryfoundation.org/poetrymagazine/articles/68950/a-sort-of-music [https://perma.cc/2CY2-5USD]. Tone painting involves “using instrumental colors, textures, dynamics (that is, how softly or loudly the music is played), and articulations that might connect the mind’s ear and eye to these images.” Id.

several questions arise as to the proper tax treatment of her creative outputs. First, should Schwendinger be considered a songwriter or a musician? Second, does it matter if she used another author’s poem in her musical composition? Third, would the tax code’s treatment of her creative outputs change if she set her original poem to music? Fourth, if Professor Schwendinger created the poem, song, and music, would the IRS consider her a poet, songwriter, or musician?

As Swift earns billions from verses describing love’s passion and pain, writers and scholars also grapple with the question of whether Swift is a poet or songwriter.

93

Madison Malone Kircher, A Harvard Professor Prepares to Teach a New Subject: Taylor Swift, N.Y. Times (Nov. 30, 2023), https://www.nytimes.com/2023/11/30/

style/taylor-swift-harvard-course.html (on file with the Columbia Law Review) (discussing Swift-inspired classes at Harvard, New York University, the University of Texas–Austin, the University of Florida, and the University of California, Berkeley). Other writers studied in the Harvard course include William Wordsworth, Samuel Taylor Coleridge, Willa Cather, and James Weldon Johnson. Id.

Swift’s Instagram post from February 4, 2024, declares that “[a]ll’s fair in love and poetry” and includes these lines:

And so I enter into evidence

My tarnished coat of arms

My muses, acquired like bruises

My talismans and charms

The tick,

tick,

tick

of love bombs

My veins of pitch black ink.

94

Swift, Instagram, supra note 6.

Here, when read aloud, Swift’s phrases pigment love’s pangs. So, is Swift a poet, songwriter, or both? American poet Eileen Myles observes that “[s]ongwriters and poets are interchangeable to some extent.”

95

Madden, supra note 2 (internal quotation marks omitted) (quoting Myles).

Professor and poet Stephanie Burt acknowledges the ongoing debate over whether Swift is a poet but argues that she “belong[s] to poetic traditions nonetheless” and appears to be inspired by “Wordsworthian romanticism, Burnsian lyricism” and Laura Kasischke’s “wit.”

96

Id. (internal quotation marks omitted) (quoting Burt); see also Kircher, supra note 93; Laura Kasischke, Poetry Found., https://www.poetryfoundation.org/poets/laura-kasischke [https://perma.cc/6TD5-Q2VL] (last visited Oct. 20, 2024) (describing Kasichke’s work as a poet and novelist as characterized by an “innovative use of narrative”).

Yet in an essay penned after the release of Swift’s album, The Tortured Poets Department, poet and literary critic Adam Kirsch considers her breakup song lyrics in light of the tortured poet archetype—that is, a “dark, brooding, [and] emotionally tormented” soul.

97

Adam Kirsch, Taylor Swift Isn’t a Tortured Poet, Wall St. J. (Apr. 23, 2024), https://www.wsj.com/arts-culture/books/taylor-swift-isnt-a-tortured-poet-ce4b8a52?mod=hp_listc_pos3 (on file with the Columbia Law Review); see also Mark Richardson, ‘The Tortured Poets Department’ Review: Taylor Swift’s Songs of the Self, Wall St. J. (Apr. 23, 2024), https://www.wsj.com/arts-culture/music/the-tortured-poets-department-review-taylor-swift-jack-antonoff-aaron-dessner-matty-healy-452feecb?mod=hp_listc_pos2 (on file with the Columbia Law Review) (observing that “[t]he pop superstar’s lengthy new album is a logorrheic account of her personal dramas, with a shortage of the memorable hooks and accessible lyrics that made her famous”).

He next contrasts Swift’s public triumphs over her romantic struggles with the intense psychological suffering that ended Sylvia Plath’s and Anne Sexton’s lives.

98

Kirsch, supranote 97; see also Anne Sexton (1928–1974), Poetry Found., https://www.poetryfoundation.org/poets/anne-sexton [https://perma.cc/3BDG-PB4B] (last visited Oct. 20, 2024) (describing how Sexton “struggled with depression” and spent time in psychiatric hospitals prior to her death by suicide at age forty-five); Sylvia Plath (1932–1963), Poetry Found., https://www.poetryfoundation.org/poets/sylvia-plath[https://perma.cc/PJA9-JP9N] (last visited Oct. 20, 2024) (“Plath’s poems explore her own mental anguish, her troubled marriage to fellow poet Ted Hughes, her unresolved conflicts with her parents, and her own vision of herself.”).

He then concludes that Swift is a glamorous and successful pop star who “only play[s]” the role of a poet.

99

Kirsch, supra note 97.

Fortunately for Swift, the tax code’s treatment of the sale of her self-created works does not depend on the conclusions of poets, professors, or literary critics. Under current law, if she catalogs and sells her self-created musical works, she suffers no tax “bruises” for her “muses”

100

Swift, Instagram, supra note 6.

since she may elect preferential capital gains treatment under I.R.C. § 1221(b)(3).

Given that current U.S. tax laws favor songs over poems, perhaps the dictionary supports the disparate treatment of poems not set to music versus poems set to music. But as discussed in the next section of this Piece, basic dictionary definitions scuttle such reasonable expectations and reveal the tax code’s tin ear.

C. Disharmonious Dictionary Definitions

The Merriam-Webster Dictionary defines “poems” as compositions in verse.

101

Poem, Merriam-Webster, https://www.merriam-webster.com/dictionary/poems [https://perma.cc/84NE-SQPX] (last visited Oct. 18, 2024). Wikipedia’s description of poetry provides some additional detail:

Poetry (from the Greek word poiesis, “making”) is a form of literary art that uses aesthetic and often rhythmic qualities of language to evoke meanings in addition to, or in place of, literal or surface-level meanings. Any particular instance of poetry is called a poem and is written by a poet.

Poetry, Wikipedia, https://en.wikipedia.org/wiki/Poetry [https://perma.cc/T57Y-6F9G] (footnotes omitted) (last visited Oct. 19, 2024).

Its broad definition of “songs,” in contrast, includes poetical compositions, short musical collections of music and words, melodies for lyric poems or ballads, and poems “easily set to music.”

102

Song, Merriam-Webster, https://www.merriam-webster.com/dictionary/songs/ [https://perma.cc/G2C3-NDDK] (last visited Oct. 19, 2024).

Based on these two definitions, the line between poems not set to music and songs (poems set to music) appears illusory and provides little support for different tax treatment of poets and songwriters.

The definition of “music,” moreover, provides little support for the preferential tax treatment of musicians who are composers, conductors, or performers. Merriam-Webster defines “music” as follows: “vocal, instrumental, or mechanical sounds having rhythm, melody, or harmony,” “the science or art of ordering tones or sounds in succession, in combination, and in temporal relationships to produce a composition having unity and continuity,” “a musical accompaniment,” and “the score . . . of a musical composition set down on paper.”

103

Music, Merriam-Webster, https://www.merriam-webster.com/dictionary/music [https://perma.cc/E5PY-X4PF] (last visited Oct. 19, 2024).

The first two definitions align with Keats’s recognition (as a composer of poetry) and Sun Ra’s realization (as a composer of poetry and music, a “jazz innovator,” and a “cosmic bandleader”) of the fluid relationship between poems, melodies, and music.

104

See supra notes 42–46 and accompanying text.

Merriam-Webster’s third musical accompaniment definition refers to “an instrumental or vocal part designed to support or complement a melody.”

105

Accompaniment, Merriam-Webster, https://www.merriam-webster.com/

dictionary/accompaniment [https://perma.cc/EF73-YRY7] (last visited Oct. 19, 2024).

The last definition involves setting the notes of a composition on paper. Because musical accompaniment and scoring function as supportive—not primary—artistic roles, it makes little sense for these ancillary creators to receive preferential tax treatment as compared to the key creators of artistic compositions.

Given that current U.S. tax laws favor songs over poems, should an artist’s tax bill depend on their art form?

D. Tax Fairness

Scrutiny of tax policies often focuses on whether similarly situated taxpayers are treated consistently.

106

See Nguyen & Maine, supra note 52, at 553–54 (explaining horizontal equity and tax fairness).

Taxpayers’ income offers a starting point for analysis. Unfortunately, a direct comparison of the annual earnings of songwriters and poets is unavailable, making it necessary to string together several sources. The U.S. Bureau of Labor Statistics (BLS) reported that the 2023 median annual wage of music directors and composers (all types) was $62,940, while the annual wage of writers and authors was $73,690.

107

Occupational Outlook Handbook: Music Directors and Composers, U.S. Bureau of Lab. Stats., https://www.bls.gov/ooh/entertainment-and-sports/music-directors-and-composers.htm#tab-5 (on file with the Columbia Law Review) (last modified Aug. 29, 2024) [hereinafter Occupational Outlook Handbook: Music Directors and Composers]; Occupational Outlook Handbook: Writers and Authors, U.S. Bureau of Lab. Stats., https://www.bls.gov/ooh/media-and-communication/writers-and-authors.htm#tab-5 (on file with the Columbia Law Review) (last modified Aug. 29, 2024).

Notably, musical artists earned $16.46 per hour, or $32,240 annually, on the low end of the scale.

108

See Occupational Outlook Handbook: Music Directors and Composers, supra note 107 (reporting that, in 2023, music directors and composers earned between $16.46 and $83.56 per hour, or between $32,240 and $173,810 annually).

Songwriters may also earn royalties and enjoy professional recognition from being named in a performer’s liner notes or album credits.

109

See Bernstein, supra note 76 (describing how piracy has harmed songwriters because of how their benefits come from song credits).

There is scant data on the income poets earn from their creative works. But the website ZipRecruiter suggests that U.S. poets make an average hourly wage of $18.75, or approximately $39,000 per year.

110

Poet Salary, ZipRecruiter, https://www.ziprecruiter.com/Salaries/Poet-Salary#Yearly (on file with the Columbia Law Review) (last visited Jan. 17, 2025) (indicating that U.S. poets earn between $21,500 and $73,500 per year).

Poets may supplement their income with prizes and awards. As a result of philanthropist Ruth Lilly’s 2002 bequest of $100,000,000,

111

Nick Paumgarten, A Hundred Million, New Yorker (Nov. 24, 2002), https://www.newyorker.com/magazine/2002/12/02/a-hundred-million (on file with the Columbia Law Review); see also Julia M. Klein, A Windfall Illuminates the Poetry Field, and Its Fights, N.Y. Times (Nov. 12, 2007), https://www.nytimes.com/2007/11/12/

giving/12POETRY.html (on file with the Columbia Law Review) (noting that the Foundation used Lilly’s donation to create “a lively, award-winning Web site with poetry podcasts and a poetry best-seller list, a reinvigorated magazine, a set of unusual prizes and . . . the Poetry Out Loud national high school recitation contest”). Id. One such aspiring poet, Ruth Lilly, showed her gratitude by endowing poetry prizes and fellowships long before her $100,000,000 bequest. Id.; see also Trib. News Servs., Poetry Gift Just Part of Heiress’ Philanthropic Promises, Chi. Trib. (Nov. 24, 2002), https://www.chicagotribune.com/

2002/11/24/poetry-gift-just-part-of-heiress-philanthropic-promises/ (on file with the Columbia Law Review) (last updated Aug. 20, 2021) (observing the connection between Poetry Magazine’s gentle rejection of Lilly’s verses over the years and her generous financial gifts).

the Poetry Foundation supports the “poetry ecosystem in perpetuity” by granting fellowships and awarding prizes between $100 and $100,000.

112

Reports and Financials, Poetry Found., https://www.poetryfoundation.org/

reports-financials [https://perma.cc/M2W3-FX9G] (last visited Oct. 20, 2024); see also The Poetry Found., 2022 Return of Private Foundation (Form 990-PF) 17–57 (Nov. 10, 2023), https://s3-us-east-2.amazonaws.com/cdn-test.poetryfoundation.org/content/documents/2022-990-PF-Poetry-Foundation.pdf [https://perma.cc/6G7M-9DTD] (summarizing the Foundation’s prize, fellowship, and grant awards that range between $100 and $100,000).

Further, the Ruth Lilly Poetry Prize honors living U.S. poets with a $100,000 award for their accomplishments.

113

Ruth Lilly Poetry Prize, Poetry Found., https://www.poetryfoundation.org/

awards/prizes-lilly [https://perma.cc/D8PF-TEXV] (last visited Oct. 18, 2024) (stating that “the prize is one of the most prestigious awards given to American poets”).

Similar to songwriters, poets may earn royalties from the sale of their compositions.

If the sun and stars cosmically align, some poets secure earthly fame and fortune—and even interplanetary preeminence. For example, after becoming the first National Youth Poet Laureate, Amanda Gorman read her poetry at the presidential inauguration, and as a result, she swiftly garnered critical and commercial success with her subsequent books and poems.

114

Amanda Gorman, https://amandagormanbooks.com/ [https://perma.cc/C8J8-PJSG] (last visited Oct. 18, 2024); see also Petra Mayer, After Inaugural Performance, Poet Amanda Gorman Tops the Amazon Bestseller List, NPR (Jan. 21, 2021), https://www.npr.org/2021/01/21/959160843/after-inaugural-performance-poet-amanda-gorman-tops-the-amazon-bestseller-list [https://perma.cc/7533-RQ97]; cf. supra text accompanying notes 83–84 (describing how, in recent years, Bob Dylan, Bruce Springsteen, Paul Simon, Neil Young, Stevie Nicks, and others made savvy business decisions to sell their catalogs for millions of dollars).

Likewise, Ada Limón, the twenty-fourth Poet Laureate of the United States and 2023 MacArthur Fellow, has been called a “unicorn” since she is a professional poet who “makes a living off her poetry.”

115

Elizabeth A. Harris, Ada Limón Makes Poems for a Living, N.Y. Times (May 6, 2022), https://www.nytimes.com/2022/05/06/books/ada-limon-poetry.html (on file with the Columbia Law Review) (describing Limón as a “unicorn” who is not a teacher, “has no day job,” and is not independently wealthy). U.S. Poet Laureate Consultant selectees receive a $35,000 annual stipend funded by philanthropist and poet Archer M. Huntington. Poet Laureate: History of the Position, Libr. of Cong., https://www.loc.gov/programs/poetry-and-literature/poet-laureate/poet-laureate-history/ [https://perma.cc/HBH3-TYV5] (last visited Oct. 18, 2024); see also Meredith Howard, The Next US Poet Laureate Has KY Roots. What to Know About the Prestigious Position, Lexington Herald Leader (July 12, 2022), https://www.kentucky.com/news/state/kentucky/article263388863.html (on file with the Columbia Law Review) (describing the annual and travel stipends that the Poet Laureate receives); United States Poet Laureate, Poets.org, https://poets.org/united-states-poet-laureate [https://perma.cc/26Z5-AWAR] (last visited Oct. 18, 2024) (naming all of the Poet Laureates of the United States). The MacArthur Fellowship recipients receive an award of $800,000 (paid out over five years in equal quarterly installments). MacArthur Fellows, MacArthur Found., https://www.macfound.org/programs/awards/fellows/about [https://perma.cc/592G-6Z8F] (last visited Oct. 18, 2024) (describing the “no-strings attached” fellowship awards).

Limón’s 2023 poem, In Praise of Mystery: A Poem for Europa, currently voyages to Europa, Jupiter’s icy moon, inside NASA’s Europa Clipper orbiter.

116

See Europa Clipper, NASA, https://science.nasa.gov/mission/europa-clipper/ [https://perma.cc/4WNX-6XTX] (last visited Oct. 18, 2024) (stating that the Europa Clipper will travel 1.8 billion miles to Jupiter’s icy moon, Europa, to determine whether it “has conditions suitable to support life”); Monika Luabeya, U.S. Poet Laureate Ada Limón Unveils Poem for Europa Clipper, NASA (June 2, 2023), https://www.nasa.gov/image-article/u-s-poet-laureate-ada-limon-unveils-poem-for-europa-clipper/ [https://perma.cc/

6ZRM-SLA4] (“The poem will be engraved on a plaque carried aboard the Europa Clipper spacecraft as part of NASA’s ‘Message in a Bottle’ campaign . . . .”). Here is Ada Limón’s poem on its way to Jupiter’s moon, Europa:

Arching under the night sky inky

with black expansiveness, we point

to the planets we know, we

pin quick wishes on stars. From earth,

we read the sky as if it is an unerring book

of the universe, expert and evident.

Still, there are mysteries below our sky:

the whale song, the songbird singing

its call in the bough of a wind-shaken tree.

We are creatures of constant awe,

curious at beauty, at leaf and blossom,

at grief and pleasure, sun and shadow.

And it is not darkness that unites us,

not the cold distance of space, but

the offering of water, each drop of rain,

each rivulet, each pulse, each vein.

O second moon, we, too, are made

of water, of vast and beckoning seas.

We, too, are made of wonders, of great

and ordinary loves, of small invisible worlds,

of a need to call out through the dark.

Ada Limón, In Praise of Mystery: A Poem for Europa, Libr. of Cong. (2023), https://www.loc.gov/programs/poetry-and-literature/poet-laureate/poet-laureate-projects/a-poem-for-europa/ [https://perma.cc/3SZX-CYH9].

When poets like Gorman and Limón sell their poems and other artistic compositions, they are subject to ordinary income tax rates. If they instead sang (rather than recited) their verses, they could potentially elect capital gains treatment—an opportunity available to the Tenth Poet Laureate of Colorado, Andrea Gibson.

117

2023–2025 Poet Laureate Andrea Gibson, Colo. Humans., https://coloradohumanities.org/programs/colorado-poet-laureate/ [https://perma.cc/

5TMP-4WZ5] (last visited Oct. 18, 2024). Gibson is a “spoken word” queer and nonbinary poet who writes about mental health, love, and social justice. See Andrea Gibson, About, Things That Don’t Suck, https://andreagibson.substack.com/about [https://perma.cc/K4GE-HEXE] (last visited Oct 18, 2024).

In addition to publishing poems, Gibson seamlessly bridges the space between poetry and song by interweaving words with music in their spoken word performance art.

118

Andrea Gibson’s books are available online. See Books, Andrea Gibson, https://store.andreagibson.com/collections/books [https://perma.cc/B6EP-VFSR] (last visited Oct. 18, 2024). Andrea Gibson’s albums are available on multiple platforms such as Apple and Amazon music. See Andrea Gibson, Wikipedia, https://en.wikipedia.org/wiki/Andrea_Gibson [https://perma.cc/J86S-3NDU] (last visited Oct. 18, 2024) (listing their books and discography).

One hopes that Gibson’s tax preparer distinguishes between income derived from poems and songs so that ordinary and capital gains tax rates can be apportioned in a catalog sale.

As previously discussed, current tax policy forms a Frankenstein’s monster that rewards musicians and songwriters with special tax benefits. U.S. tax laws should not pick winners and losers just because their favorite musicians or songwriters serenaded them in their congressional office.

119

See Bernstein, supra note 76 (stating that the Nashville Songwriters Association International made over twenty trips to Washington to lobby Congress).

Simply put, current tax laws breed “bad blood”

120

Taylor Swift, Bad Blood, on 1989 (Big Machine Recs. 2014).

between musicians, other artists, and regular wage earners.

E. Poetry and Principled Legislation

As this Piece’s examination of the I.R.C.’s clashing treatment between poems and songs closes, the fact remains that Congress created this tax policy monstrosity. In his 1821 essay, the British Romantic poet and writer Percy Bysshe Shelley observed that “[p]oets are the unacknowledged legislators of the world”

121

Shelley, A Defence of Poetry, supra note 4, at 1146. Shelley closes A Defence of Poetry by describing how poetry can be a force for change and good:

Poets are the hierophants [priests or expositor] of an unapprehended inspiration; the mirrors of the gigantic shadows which futurity casts upon the present; the words which express what they understand not; the trumpets which sing to battle, and feel not what they inspire; the influence which is moved not, but moves. Poets are the unacknowledged legislators of the world.

Id. (footnote omitted).

because their insights and imaginations can serve as “great instrument[s] of moral good.”

122

Id. at 1136.

If future Congresses are committed to enacting tax laws that are principled and coherent, the following questions can help guide their analyses and actions toward artist tax equity:

Should the favorable tax treatment of songs and music be retained or eliminated?

If the preferential tax treatment of songs and music is merited, should there be limits on the amount of income eligible for capital gains treatment? For example, should taxpayers be eligible for a specific dollar amount (e.g., up to $100,000) in capital gains treatment, with the balance subject to ordinary income rates?

123

See, g., Taite, supra note 86, at 1028 (proposing “to limit preferential rates on capital property to taxpayers earning $100,000 or less”).

If preferential tax treatment of songs and music is merited, should taxpayers be required to hold the property for a specified time?

124

See, e.g.,R.C. § 724 (2018) (setting out a five-year holding period for inventory items).

What constitutes self-created musical compositions or works?

125

See Morris, supra note 62.

How should each contributor–taxpayer be taxed if a poet and a musician collaborate on a new composition?

126

See id.

How should each contributor–taxpayer be taxed if a taxpayer already published (and copyrighted) a poem and later joins forces with a musician to intertwine their verses into a new musical work (a song)?

127

See id.; see also Schwendinger, supra note 92 (raising the question of whether using another author’s poem through tone painting results in the artist being classified as a song writer or musician for tax purposes).

How should an artist who is both a poet and musician be taxed if the artist creates both poems and songs?

128

See, e.g., Abrams, supra note 47, at 3 (noting that at “Cornell, a famed English professor, Hiram Corson, read poems aloud in Sage Chapel accompanied by the chapel organ, to high acclaim”); supra notes 114–116 and accompanying text.

Is the IRS qualified to ascertain whether a work product should be treated as a poem or a song?

129

See Jenkins v. Comm’r, 47 T.C.M. (CCH) 238, at *32 n.14 (1983) (closing the memorandum with an “Ode to Conway Twitty,” summarizing the facts and opinion in the structure of a song or poem). While the IRS’s counter in the Jenkins case represents a valiant effort by tax nerds, characterizing it as poetry is a stretch.

Will the IRS evaluate the substance and form of artistic works that strategically include sound so the taxpayer may elect favorable tax treatment as a musical composition?

Should all self-created artistic works—no matter the form—be taxed fairly and consistently?

Conclusion

While the U.S. tax code will never be a cozy “cardigan,”

130

Taylor Swift, Cardigan, on Folklore (Republic Recs. 2020).

it can at least be coherent. For defenders of the tax status quo who say, “You need to calm down,”

131

Taylor Swift, You Need to Calm Down, on Lover (Republic Recs. 2019).

the issue remains of whether the advantageous tax treatment of musical compositions and copyrights is justified over poems that also fill “blank space[s]”

132

Taylor Swift, Blank Space, on 1989 (Big Machine Recs. 2014).

with heartfelt, insightful, and clever turns of phrase. At this time, the evidence shows that the I.R.C. is a “tax Frankenstein,” bizarrely stitched together with tax benefits that serve the special interests of select groups.

The “pitch black ink”

133

Swift, Instagram, supra note 6.

of the tax code reveals two sharp truths: First, tax fairness does not extend to those who write love poems—only to those who write love songs. Second, ticking tax—not love—bombs may explode on less congressionally-favored artists who sell their creative works.

134

Id.

Congress must slay its tax monster so that love songs, stories, poems, and other artistic works are taxed harmoniously in a “state of grace.”

135

Taylor Swift, State of Grace, on Red (Republic Recs. 2012).